There is a lot more to buying a home than just affording the solicitor’s costs, removal fees and mortgage repayments. We all know this, but what about other key outgoings? How would you cope if interest rates rose?

Back in April the government changed the rules on mortgage lending. Now, if you want to buy a home you’ll need to provide your lender with much more information before they’ll consider your application for a loan.

So if you’re in the market for a new property, you’ll really need to make sure your paperwork is in order to get through the newly beefed-up affordability checks.

The changes mean the process of getting a mortgage is lengthier and more forensic, and you’ll be asked about things like household expenses and utility bills in much more detail than before.

Why the rules were introduced

The rules are intended to stop borrowers overstretching themselves – something three in four first-time buyers admitted to in a survey by the Money Advice Service.

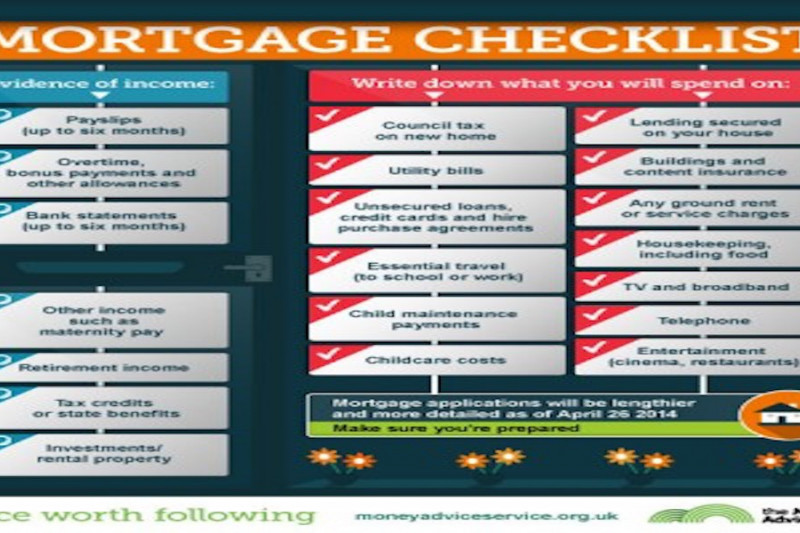

Whether you’re a first-time buyer or just looking to remortgage, you’ll be asked to provide evidence of your income as part of the application process.

This will include, among other things:

- Payslips

- Bank statements going back at least three months, maybe more

- Evidence of retirement income

- Evidence of maternity pay.

If you have rental properties or other investments you’ll need to be prepared with details of those too.

The changes don’t just focus on income though. You will need a clear – probably written down - idea of your household budget, everything from council tax and electricity through to what you plan to spend on things like television and broadband.

In addition you should be prepared to provide evidence of and discuss the following:

- Any loans you have, and your repayment record

- Any credit cards you have, and your current balance

- Accounting for future events

You’ll also need to be ready to show how you’d cope with increased costs, caused by things like interest rate rises, or if you have a change of personal circumstance on the horizon – say retirement, or having a baby.

Lenders will have to ‘stress-test’ your finances to make sure they won’t break if costs go up. For example, homeowners with a £140,000 mortgage, making monthly repayments of £749 at 3.4% APR, would have to find an additional £171 a month if interest rates were to rise by 2%.

Time well spent

The reality is the tightened up rules could affect the amount of money you’re able to borrow to get your dream home.

You can expect to have at least one meeting with your mortgage lender to discuss your finances, with the initial consultation lasting more than one hour, so it will really pay to do your homework and turn up well prepared to answer all their questions.

If you get the mortgage you want you can rest assured you are well placed to afford what is the biggest financial commitment of your life.

The Money Advice Service has produced a Mortgage Market Review guide on the changes, which includes more information on what you’ll need to know if you’re planning to buy a home.

Source: Rightmove.co.uk